|

Posted: 11/13/2011 7:19:12 AM EDT

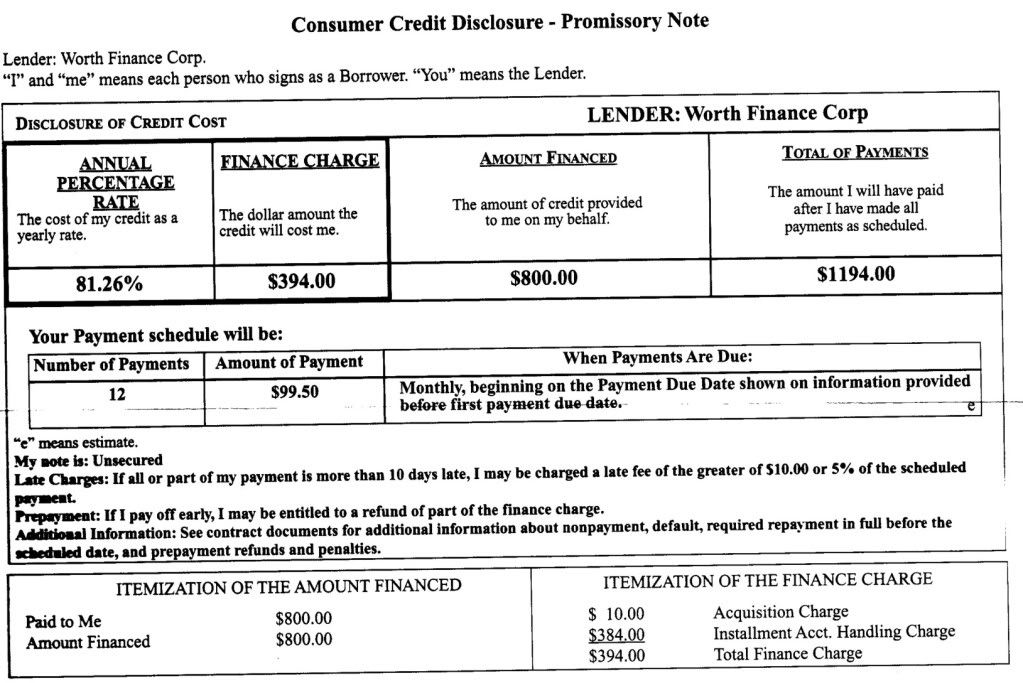

Perhaps I'm a bit slow this morning, but I don't understand how this 81.26% APR is calculated:

And no worries, I'm not about to bite - it's just from some junk mail. |

|

|

|

[#1]

Wow, that's an awesome deal.

|

|

|

|

[#2]

I think I'd shit in the envelope and return it. |

|

|

|

[#3]

I got one of those. Said there was a "low" annual fee of $95

for a credit line of $500. No setup charges but had some sort of "document charge" of $200. I was wondering what fucking idiot would do this. The rate was insane as well.

|

|

|

|

[#4]

Oh I agree that it's a turd of a deal, something nobody in their right mind would do in their real name.

But still, the way I read it the APR is more like (an also outrageous) 49.25%. How do they get 81.26%? |

|

|

|

[#5]

I think the same way they figured out how to fit 40lbs of Rape in a box.

|

|

|

|

[#6]

Quoted:

I think the same way they figured out how to fit 40lbs of Rape in a box legal-sized envelope. FIFY |

|

|

|

[#7]

APR = interest rate of the loan, plus the fees paid to the lender (at the inception, at the end, etc) as if the fees were not paid in lump sum but instead spread over the life of the loan.

You'd need to see all he fees for the APR to "make sense". I look at loan docs all day and the APR is pretty much useless, other than to tell you which loan is a better deal. When the APR is vastly different than your stated interest rate, it means that there are a bunch of fees, or credits. |

|

|

|

[#8]

Quoted:

Oh I agree that it's a turd of a deal, something nobody in their right mind would do in their real name. But still, the way I read it the APR is more like (an also outrageous) 49.25%. How do they get 81.26%? If the loan has negative amortization, I believe the calc is different. Too lazy to open Excel to figure out... |

|

|

|

[#9]

I don't see how it could involve negative amortization if it's paid off in a year.

ETA - I guess it must have something to do with late payment fees(?). The only other fee mentioned is the $1.00 Acquisition Charge. |

|

|

|

[#10]

It is because you are not financing 800 dollars for a year, you are financing 800 dollars for the first month, after that you are financing a smaller amount every month.

|

|

|

|

[#11]

Only way it makes sense to me is if the loan is due in full in 6 months. 40% int rate over 6 mos is 80& annually.

|

|

|

|

[#12]

Some car loans used to be like that - Rule of 78s IIRC - where if you paid it off in the first couple of months you'd find out your first few payments had barely scratched the prinicipal.

|

|

|

|

[#13]

You can judge a man by the quality of his junk mail.

I got nothing

|

|

|

|

[#14]

Quoted:

You can judge a man by the quality of his junk mail. More people want me to give them money than want to give me money. |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.