USA

|

Posted: 2/9/2024 7:10:46 PM EDT

[Last Edit: Switchback_Arms]

Reading The Simple Path to Wealth and I'm considering consolidating most if not all my 401k to the Fidelity equivalent of VTSAX.

It looks like FSKAX might tbe the closest but then I noticed their Zero funds like FZROZ and FNILX. Seems cool that they have zero fees but FSKAX has very low fees and I think pays more. What say all you? Which one is the best? I have a healthy risk appetite, just want to dump it, contribute and not pay attention to it. Also, The Simple Path to Wealth guy seems like a proponent of traditional 401ks vs Roth 401ks. I've always done Roth and am still leaning that way. What do you all think? Obviously you can tell I'm no guru on this stuff, just looking for some more opinions. Thanks |

|

|

|

[#1]

I use FXAIX. S&P500 mutual fund as opposed to the total US fund. Better returns and lower expense ratio.

|

|

|

|

|

[#2]

there are issues with the ZERO funds.

choose wisely. |

|

|

|

|

[#3]

Originally Posted By Jarcese: I use FXAIX. S&P500 mutual fund as opposed to the total US fund. Better returns and lower expense ratio. This is the way. I have pretty much everything in FXIAX. |

|

|

|

USA

|

[#4]

Originally Posted By OKnativeson: This is the way. I have pretty much everything in FXIAX. Originally Posted By OKnativeson: Originally Posted By Jarcese: I use FXAIX. S&P500 mutual fund as opposed to the total US fund. Better returns and lower expense ratio. This is the way. I have pretty much everything in FXIAX. Oh cool, I didn't see that one. It's not on my list, may have to do a brokeragelink to do it. |

|

|

|

[Last Edit: djkest]

[#5]

Originally Posted By Switchback_Arms: Reading The Simple Path to Wealth and I'm considering consolidating most if not all my 401k to the Fidelity equivalent of VTSAX. It looks like FSKAX might tbe the closest but then I noticed their Zero funds like FZROZ and FNILX. Seems cool that they have zero fees but FSKAX has very low fees and I think pays more. What say all you? Which one is the best? I have a healthy risk appetite, just want to dump it, contribute and not pay attention to it. Also, The Simple Path to Wealth guy seems like a proponent of traditional 401ks vs Roth 401ks. I've always done Roth and am still leaning that way. What do you all think? Obviously you can tell I'm no guru on this stuff, just looking for some more opinions. Thanks I have a Fidelity 401k I use Fidelity Brokeragelink to buy VTSAX while keeping the money in the 401k. EDIT: I was incorrect, in my Fideltiy brokeragelink account I am holding QQQ and VUG; But you could buy VTSAX |

|

|

|

|

[#6]

Originally Posted By djkest: I have a Fidelity 401k I use Fidelity Brokeragelink to buy VTSAX while keeping the money in the 401k. EDIT: I was incorrect, in my Fideltiy brokeragelink account I am holding QQQ and VUG; But you could buy VTSAX Buying Vanguard MF's through Fidelity Brokeragelink usually results in a $75 fee when you buy. If you're gonna use Brokeragelink, buy VTI, which is the ETF equivalent of VTSAX. With Fidelity, if you don't want to use a ZERO fund, FSKAX is Fidelity's total market index fund. |

|

|

|

|

[#7]

Originally Posted By OKnativeson: there are issues with the ZERO funds. choose wisely. |

|

|

|

|

[Last Edit: OKnativeson]

[#8]

Originally Posted By Sartorius: Which issues do you see? Is it the fact that FZROX tracks the Fidelity US Total Investable Market Index, which is a bit non-standard? Or something else? the Devil is in the details on these new ZERO funds. one- from my understanding, you cannot transfer these funds later on. they are basically Fidelity forever. two- I don't think the stocks and companies in these Funds are the same and or in % as the main Fidelity Funds. there are probably more issues that I'm not aware of. if I'm wrong on this topic, I apologize. but I looked into them when they came out. |

|

|

|

|

[#9]

FZROX holds around 2600 stocks, while VTSAX holds about 3750. Maybe slightly less diversity, but with the fee savings, I'd say it's worth it. Even a miniscule fee can add up over time.

|

|

|

|

USA

|

[#10]

So what would all pick for Fidelity? FXIAX, FZROX or FSKAX?

FXIAX - Fidelity 500 Index Fund - 0.015% FZROX - Fidelity ZERO Total Market Index Fund - Expense Ratio 0.00% FSKAX - Fidelity Total Market Index Fund - Expense Ratio 0.02% That's about all I understand about the differences. All seem good to me compared to VTSAX at 0.040% plus extra Fidelity fees. Is it the dividends that make one better than the other? Basically I'm trying simplify and streamline all my investments and put them on autopilot. Thanks! |

|

|

|

[Last Edit: FALARAK]

[#11]

FSKAX = VTSAX

I use FSKAX or VTI at Fidelity. I use VTI mostly because I can trade during the day if ever needed as it is an ETF, and it is *slightly* more tax efficient for taxable brokerage accounts. In accounts that do not allow VTI (such as my HSA) I use FSKAX. In accounts that do not have a "Total US Equities market index fund" I use the S&P500 fund they almost always offer. FZROX is more of a gimmick, it will net the same as FSKAX, it was just a marketing compete to say "we have zero expense funds too". I dont have a problem with it, but I do not choose it over FSKAX. One you are looking at expense ratios under 0.05%, comparing them at that low of a level is miniscule. You need to avoid large expense ratios on funds.... but 0.015 vs 0.04 should not be a distinguishable investment choice. |

|

|

|

|

[#12]

Originally Posted By OKnativeson: the Devil is in the details on these new ZERO funds. one- from my understanding, you cannot transfer these funds later on. they are basically Fidelity forever. two- I don't think the stocks and companies in these Funds are the same and or in % as the main Fidelity Funds. there are probably more issues that I'm not aware of. How often do you move a retirement or brokerage account? I've rolled over one pre-tax account in my entire life and have never moved a post-tax account. If you're moving pre-tax then it doesn't matter if you can keep the funds or not. If you have so much post-tax profit that it's a concern then you're doing so well it's really just an issue that you can work into your overall financial plan. All funds are different, you can read up on how they achieve their goals. Just being different from some other random fund isn't automatically bad(or good). The biggest issue is that if you want to invest-and-forget for the long term a zero fund can be a very powerful tool. Do the math over the difference in return on 0 fees vs a low fee of 0.05 vs a high fee of 0.5-1.0. If you're investing in your 20s for retirement that is 30-50 years away the lower fees can make a huge difference. I think the zero fee funds are mainly a way to get money into fidelity - they obviously make no income from the funds, but once a customer is attracted by the zero-fee funds that customer brings ancillary business into fidelity because it's easier than using multiple brokerages. |

|

|

|

|

[Last Edit: Skar]

[#13]

I retired and put 65%of my money in Vanguard VOO similar, but a ETF

Can buy your sell on the spot don’t have to wait till closing price like a mutual fund .( buy sell anytime market hours) |

|

|

|

|

[#14]

Originally Posted By Switchback_Arms: So what would all pick for Fidelity? FXIAX, FZROX or FSKAX? FXIAX - Fidelity 500 Index Fund - 0.015% FZROX - Fidelity ZERO Total Market Index Fund - Expense Ratio 0.00% FSKAX - Fidelity Total Market Index Fund - Expense Ratio 0.02% That's about all I understand about the differences. All seem good to me compared to VTSAX at 0.040% plus extra Fidelity fees. Is it the dividends that make one better than the other? Basically I'm trying simplify and streamline all my investments and put them on autopilot. 0 vs 0.02 vs 0.04 fees are so low that they're negligible. I would suggest that the big difference is fxaix (sp500 index) vs the other three (all total market indexes). Without confirming, I would expect the sp500 to outperform the total market in the long-term. I'll check, please hold..... Yes, fxaix has outperformed the other three over all timeframes. The total stock market has lots of dumpy companies and penny stocks that drag down average performance. A sp500 fund only invests in the sp500 companies, and low-performing stocks aren't in the sp500 so you don't have their deadweight in your investment. Of the four you listed I would put 100% in fxaix. Also that's what Warren Buffet recommends so you can't go wrong with that. |

|

|

|

|

[#15]

Originally Posted By Morgan321: How often do you move a retirement or brokerage account? I've rolled over one pre-tax account in my entire life and have never moved a post-tax account. If you're moving pre-tax then it doesn't matter if you can keep the funds or not. If you have so much post-tax profit that it's a concern then you're doing so well it's really just an issue that you can work into your overall financial plan. All funds are different, you can read up on how they achieve their goals. Just being different from some other random fund isn't automatically bad(or good). The biggest issue is that if you want to invest-and-forget for the long term a zero fund can be a very powerful tool. Do the math over the difference in return on 0 fees vs a low fee of 0.05 vs a high fee of 0.5-1.0. If you're investing in your 20s for retirement that is 30-50 years away the lower fees can make a huge difference. I think the zero fee funds are mainly a way to get money into fidelity - they obviously make no income from the funds, but once a customer is attracted by the zero-fee funds that customer brings ancillary business into fidelity because it's easier than using multiple brokerages. I've moved my stuff a few times due to work. why in the world would you paint you and your money into something with no escape route. |

|

|

|

USA

|

[#16]

Originally Posted By OKnativeson: I've moved my stuff a few times due to work. why in the world would you paint you and your money into something with no escape route. Originally Posted By OKnativeson: Originally Posted By Morgan321: How often do you move a retirement or brokerage account? I've rolled over one pre-tax account in my entire life and have never moved a post-tax account. If you're moving pre-tax then it doesn't matter if you can keep the funds or not. If you have so much post-tax profit that it's a concern then you're doing so well it's really just an issue that you can work into your overall financial plan. All funds are different, you can read up on how they achieve their goals. Just being different from some other random fund isn't automatically bad(or good). The biggest issue is that if you want to invest-and-forget for the long term a zero fund can be a very powerful tool. Do the math over the difference in return on 0 fees vs a low fee of 0.05 vs a high fee of 0.5-1.0. If you're investing in your 20s for retirement that is 30-50 years away the lower fees can make a huge difference. I think the zero fee funds are mainly a way to get money into fidelity - they obviously make no income from the funds, but once a customer is attracted by the zero-fee funds that customer brings ancillary business into fidelity because it's easier than using multiple brokerages. I've moved my stuff a few times due to work. why in the world would you paint you and your money into something with no escape route. Agreed, I do see that as a downside with the Zero funds now. I work in tech so changing jobs is typical. |

|

|

|

[#17]

Originally Posted By OKnativeson: I've moved my stuff a few times due to work. why in the world would you paint you and your money into something with no escape route. Originally Posted By OKnativeson: Originally Posted By Morgan321: How often do you move a retirement or brokerage account? I've rolled over one pre-tax account in my entire life and have never moved a post-tax account. If you're moving pre-tax then it doesn't matter if you can keep the funds or not. If you have so much post-tax profit that it's a concern then you're doing so well it's really just an issue that you can work into your overall financial plan. All funds are different, you can read up on how they achieve their goals. Just being different from some other random fund isn't automatically bad(or good). The biggest issue is that if you want to invest-and-forget for the long term a zero fund can be a very powerful tool. Do the math over the difference in return on 0 fees vs a low fee of 0.05 vs a high fee of 0.5-1.0. If you're investing in your 20s for retirement that is 30-50 years away the lower fees can make a huge difference. I think the zero fee funds are mainly a way to get money into fidelity - they obviously make no income from the funds, but once a customer is attracted by the zero-fee funds that customer brings ancillary business into fidelity because it's easier than using multiple brokerages. I've moved my stuff a few times due to work. why in the world would you paint you and your money into something with no escape route. Moving a tax deferred/workplace related account is a non-issue. You simply sell the assets to cash before the transfer, and repurchase the allocation you want in the new plan. There is no capital gain or loss in a tax deferred/tax free work related account. Moving a taxable account is where you might have issues, in which case you should just leave the account open with that custodian if the assets cannot transfer without sale. |

|

|

|

|

[#18]

Originally Posted By FALARAK: Moving a tax deferred/workplace related account is a non-issue. You simply sell the assets to cash before the transfer, and repurchase the allocation you want in the new plan. There is no capital gain or loss in a tax deferred/tax free work related account. Moving a taxable account is where you might have issues, in which case you should just leave the account open with that custodian if the assets cannot transfer without sale. Yeah, but it's also one more thing to deal with when you're potentially in a transition to a new job, doing interviews, possibly moving. If he forgets to do it, Fidelity might liquidate it, rather than call him (I've heard of this happening, not necessary at Fidelity) and then you're out of the market until the rollover is complete. As to Morgan's comments, he isn't wrong, but the other side of the coin is that those other 3,000+/- companies that are in VTSAX & FSKAX add to the diversification that the Total US Market funds are touted for. I prefer the Total US Market funds over the S&P500 because of that diversification, but I do have some S&P500 funds as a result of some LTCG tax harvesting, and they are fine. |

|

|

|

|

[#19]

Originally Posted By DDalton: .... the other side of the coin is that those other 3,000+/- companies that are in VTSAX & FSKAX add to the diversification that the Total US Market funds are touted for. I prefer the Total US Market funds over the S&P500 because of that diversification, but I do have some S&P500 funds as a result of some LTCG tax harvesting, and they are fine. Diversification is a gotcha word because it can be applied to anything. You're speaking about diversifying by holding stocks from a larger number of randomly selected companies. That sort of diversification can give random and unpredictable results, but in this case the result is predictable and the result is lower returns because you are actually increasing risk by adding random stocks. sp500 stocks are chosen based on their performance, so the turd stocks are filtered out and you get consistently better returns. I'll say it again: the sp500 (and all low cost sp500 funds) have outperformed vtsax and fskax over all possible time periods longer than a month. Putting money into a total stock market fund is as close to a guarantee as you can get that you will underperform the sp500 alternative. There are good reasons to hold a total market fund, but "diversification because it holds a larger number of stocks" is not a reason that is supported by any objective evidence. Coupled with your obtuse "hard to move" argument I wonder if you're just here to shit on things or are suffering from confirmation bias. |

|

|

|

|

[#20]

You should try not to be an insulting jerk. I read all the comments and try to not repeat ideas ad nauseum, but do try to offer productive ideas that are often counterpoints. Try not to get your panties in a wad... I clearly stated that you weren't wrong in what you said and clearly said that I was offering the flip side to that idea that choosing the S&P500 is only a positive thing. I also clearly stated that I own some S&P500. I noticed months ago that you seem to think your opinion is the only one that matters, and you have no hesitation to insult people who have a different idea.

There is no shortage of people that post on forums all over the internet about their concerns with the S&P500 and US Total Stock Market funds being way overweighted with the big 7 these days. You may not be concerned with that, and you clearly don't understand how all those awful mediocre stocks could ease someone's concerns, but it is a thing that people want the added diversification, nonetheless. I offered that to the discussion. I don't care if it hurts your feelings. |

|

|

|

|

[#21]

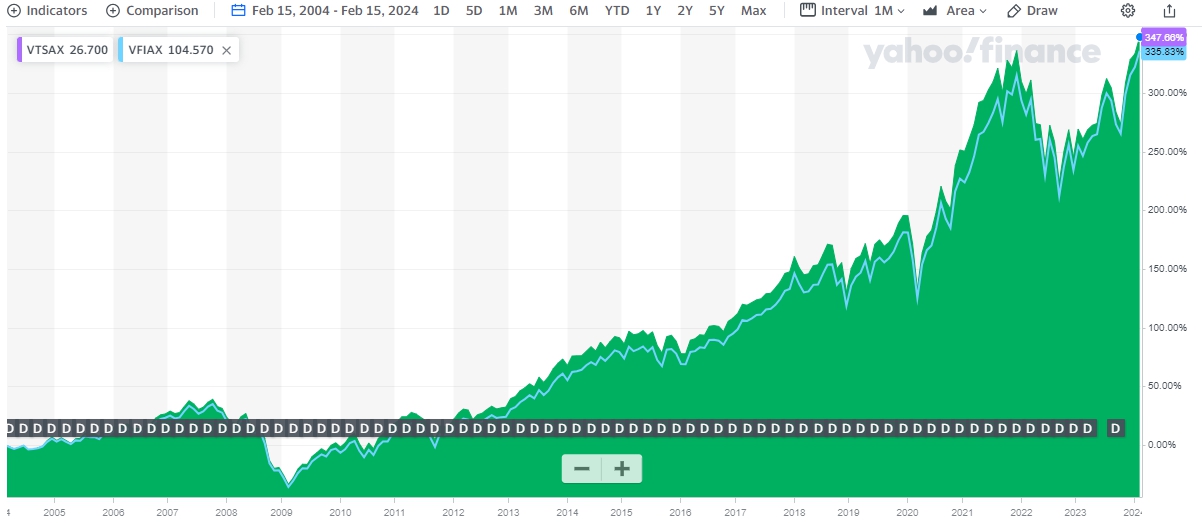

Originally Posted By Morgan321: Diversification is a gotcha word because it can be applied to anything. You're speaking about diversifying by holding stocks from a larger number of randomly selected companies. That sort of diversification can give random and unpredictable results, but in this case the result is predictable and the result is lower returns because you are actually increasing risk by adding random stocks. sp500 stocks are chosen based on their performance, so the turd stocks are filtered out and you get consistently better returns. I'll say it again: the sp500 (and all low cost sp500 funds) have outperformed vtsax and fskax over all possible time periods longer than a month. Putting money into a total stock market fund is as close to a guarantee as you can get that you will underperform the sp500 alternative. There are good reasons to hold a total market fund, but "diversification because it holds a larger number of stocks" is not a reason that is supported by any objective evidence. Coupled with your obtuse "hard to move" argument I wonder if you're just here to shit on things or are suffering from confirmation bias. Originally Posted By Morgan321: Originally Posted By DDalton: .... the other side of the coin is that those other 3,000+/- companies that are in VTSAX & FSKAX add to the diversification that the Total US Market funds are touted for. I prefer the Total US Market funds over the S&P500 because of that diversification, but I do have some S&P500 funds as a result of some LTCG tax harvesting, and they are fine. Diversification is a gotcha word because it can be applied to anything. You're speaking about diversifying by holding stocks from a larger number of randomly selected companies. That sort of diversification can give random and unpredictable results, but in this case the result is predictable and the result is lower returns because you are actually increasing risk by adding random stocks. sp500 stocks are chosen based on their performance, so the turd stocks are filtered out and you get consistently better returns. I'll say it again: the sp500 (and all low cost sp500 funds) have outperformed vtsax and fskax over all possible time periods longer than a month. Putting money into a total stock market fund is as close to a guarantee as you can get that you will underperform the sp500 alternative. There are good reasons to hold a total market fund, but "diversification because it holds a larger number of stocks" is not a reason that is supported by any objective evidence. Coupled with your obtuse "hard to move" argument I wonder if you're just here to shit on things or are suffering from confirmation bias. Here is JL Collins take on the subject: Unimportant: Whether you use a total stock market index fund or an S&P 500 index fund. Both are broad-based, low-cost funds, which is what you want. VFIAX is Vanguard’s S&P 500 index fund and it is more commonly found in 401k type plans than VTSAX. (Or the equivalents from other firms.) I prefer VTSAX, because it holds some mid-cap and small-cap stocks as well as the 500 largest. But because these funds are “cap-weighted” ~80% of VTSAX is made up of the S&P 500. If you track the performance of VTSAX v. VFIAX over 20 years the difference is tiny. Jack Bogle held VFIAX until his death. Warren Buffett has it as the investment of choice for his heirs. If it is what you have, or what you prefer, you’ll be fine with it, too. If you compare these two over the past 20 years, VTSAX ever so slightly outperformed VFIAX. So your statement that S&P500 index funds outperform Total US equity market funds across all time periods is not entirely true.  |

|

|

|

|

[#22]

Originally Posted By FALARAK: If you compare these two over the past 20 years, VTSAX ever so slightly outperformed VFIAX. So your statement that S&P500 index funds outperform Total US equity market funds across all time periods is not entirely true. Originally Posted By FALARAK: If you compare these two over the past 20 years, VTSAX ever so slightly outperformed VFIAX. So your statement that S&P500 index funds outperform Total US equity market funds across all time periods is not entirely true. Indeed it seems so. I was logged into fidelity and the info I was looking at was only available for the previous 10 years and I wasn't even looking at vfiax.... But that is interesting - also the returns for vfiax are rated "above average" while vtsax returns are "below average" despite the similarity of their returns. Originally Posted By DDalton: You should try not to be an insulting jerk...... I don't care if it hurts your feelings. OK. |

|

|

|

|

[#23]

Originally Posted By FALARAK: Moving a tax deferred/workplace related account is a non-issue. You simply sell the assets to cash before the transfer, and repurchase the allocation you want in the new plan. There is no capital gain or loss in a tax deferred/tax free work related account. Moving a taxable account is where you might have issues, in which case you should just leave the account open with that custodian if the assets cannot transfer without sale. interesting. is this legit on the ZERO funds? |

|

|

|

|

[#24]

Originally Posted By OKnativeson: is this legit on the ZERO funds? Don't know - I (quickly) scanned fidelity's website about outside investments being prohibited and found nothing, but google found a couple non-fidelity sites saying they were prohibited. Again, if true, the only time this would present an issue is if you were moving a taxable brokerage account. People move their IRA/401k all the time and, since they are tax-free until distribution, selling holdings to move the account is a non-issue. In my opinion this is a poison the well and/or boogey man argument. If true, the chance this will create a problem for anybody is so small it might as well be non-existent. |

|

|

|

FL, USA

|

[#25]

So the idea is to sell most of your stocks etc and consolidate to a SP500 fund?

|

|

|

|

[#26]

Originally Posted By OKnativeson: the Devil is in the details on these new ZERO funds. one- from my understanding, you cannot transfer these funds later on. they are basically Fidelity forever. two- I don't think the stocks and companies in these Funds are the same and or in % as the main Fidelity Funds. there are probably more issues that I'm not aware of. if I'm wrong on this topic, I apologize. but I looked into them when they came out. Potentially dumb, and definitely lazy, question - but how do they make $$ |

|

|

|

|

[#27]

Originally Posted By Pachucko: Potentially dumb, and definitely lazy, question - but how do they make $$ If they don’t charge fees then they don’t make a profit on managing the fund itself. It’s marketing - people want zero fee funds so they offer it. Then people get a fidelity account to buy it and bring other business to fidelity in the process. |

|

|

|

|

[#28]

Originally Posted By Pachucko: Potentially dumb, and definitely lazy, question - but how do they make $$ by power of the money they hold and the fact that later on those investors will become investors that graduate into other types of holdings. |

|

|

|

|

[#29]

as others have said i think the zero funds are just to get people in the door.

i have: VOO in my brokerage account. FNILX in my roth ira FXIAX in my traditional ira. they are all basically s&p500 funds. FNILX is a zero fund that is for all purposes an s&p500 fund. however my understanding is they are not allowed to use the "s&p500" in the description or they would have to pay a licensing fee to standard and poors. the funds have all move in unison. with total returns being almost identical for all available time periods. the only downside i have seen with FNILX is that it only pays out at the end of the year versus the other two paying out quarterly. if that is important to you. |

|

|

|

|

[#30]

This Zero fee Fund was created to get people to migrate to Fidelity to access the fee free fund.

If your stuff is already with Fidelity, their Zero Fund makes sense. The fund very closely mimics their Fee Fund. |

|

|

|

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.