|

[#1]

Enjoy it while it lasts.

|

|

|

|

[#2]

Quoted: You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. Only 100 days? Amateur.  I used to work with people who had 200+ days of sick leave saved up, to count as part of their years of service in their pension calculations. |

|

|

|

[#3]

Quoted: You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. Quoted: Quoted: Quoted: Quoted: Quoted: Meh. My wife’s ky pension is bringing home x a month after tax. Covers all cashout flow and still buy. And a good portion of that pension income is still buying. But tell me I’m doing it wrong. Cashflow. How do it work. Your wife brings in nearly $200k a year from a state pension? Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. NJ has one of the best pensions in the country (not saying anything about the funding level) and their pensions don't come close to that unless you possibly early 250k to 300k as a police admin. You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. What KY pension system is that? |

|

|

|

[#4]

Quoted: Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. Quoted: Quoted: Quoted: Meh. My wife’s ky pension is bringing home x a month after tax. Covers all cashout flow and still buy. And a good portion of that pension income is still buying. But tell me I’m doing it wrong. Cashflow. How do it work. Your wife brings in nearly $200k a year from a state pension? Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. Holy crap, what kind of state job generates that…please dont say teacher. |

|

|

|

[#5]

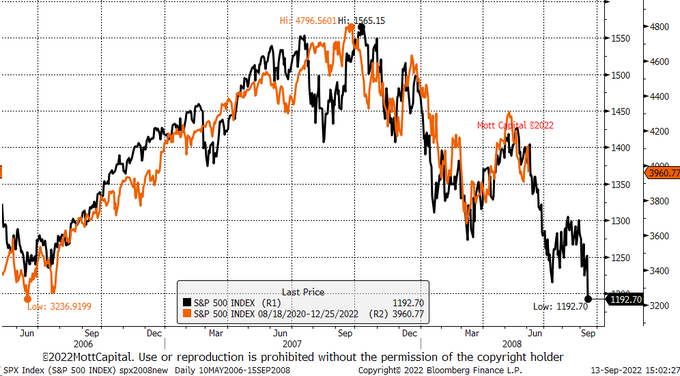

Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. |

|

|

|

[#6]

Quoted: You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. Quoted: Quoted: Quoted: Quoted: Quoted: Meh. My wife’s ky pension is bringing home x a month after tax. Covers all cashout flow and still buy. And a good portion of that pension income is still buying. But tell me I’m doing it wrong. Cashflow. How do it work. Your wife brings in nearly $200k a year from a state pension? Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. NJ has one of the best pensions in the country (not saying anything about the funding level) and their pensions don't come close to that unless you possibly early 250k to 300k as a police admin. You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. No offense because it sounds like you’ve planned well. But you sound like a couple of mine and my wife’s uncles. Or several coworkers. I heard about all their plans and preparations for years at family gatherings. Fast forward a few years and they’re dead, variety or reasons. I’m just constantly reminded of the vanity of it all. Don’t get me wrong, I’ve planned but never discuss it really. Our country is circling the drain. |

|

|

|

[#7]

Quoted: No offense because it sounds like you’ve planned well. But you sound like a couple of mine and my wife’s uncles. Or several coworkers. I heard about all their plans and preparations for years at family gatherings. Fast forward a few years and they’re dead, variety or reasons. I’m just constantly reminded of the vanity of it all. Don’t get me wrong, I’ve planned but never discuss it really. Our country is circling the drain. Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Meh. My wife’s ky pension is bringing home x a month after tax. Covers all cashout flow and still buy. And a good portion of that pension income is still buying. But tell me I’m doing it wrong. Cashflow. How do it work. Your wife brings in nearly $200k a year from a state pension? Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. NJ has one of the best pensions in the country (not saying anything about the funding level) and their pensions don't come close to that unless you possibly early 250k to 300k as a police admin. You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. No offense because it sounds like you’ve planned well. But you sound like a couple of mine and my wife’s uncles. Or several coworkers. I heard about all their plans and preparations for years at family gatherings. Fast forward a few years and they’re dead, variety or reasons. I’m just constantly reminded of the vanity of it all. Don’t get me wrong, I’ve planned but never discuss it really. Our country is circling the drain. Im here for a good time, not a long time! |

|

|

|

[#8]

Quoted: Im here for a good time, not a long time! Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Meh. My wife’s ky pension is bringing home x a month after tax. Covers all cashout flow and still buy. And a good portion of that pension income is still buying. But tell me I’m doing it wrong. Cashflow. How do it work. Your wife brings in nearly $200k a year from a state pension? Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. NJ has one of the best pensions in the country (not saying anything about the funding level) and their pensions don't come close to that unless you possibly early 250k to 300k as a police admin. You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. No offense because it sounds like you’ve planned well. But you sound like a couple of mine and my wife’s uncles. Or several coworkers. I heard about all their plans and preparations for years at family gatherings. Fast forward a few years and they’re dead, variety or reasons. I’m just constantly reminded of the vanity of it all. Don’t get me wrong, I’ve planned but never discuss it really. Our country is circling the drain. Im here for a good time, not a long time! YOFO |

|

|

|

[#9]

Quoted: What KY pension system is that? Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Meh. My wife’s ky pension is bringing home x a month after tax. Covers all cashout flow and still buy. And a good portion of that pension income is still buying. But tell me I’m doing it wrong. Cashflow. How do it work. Your wife brings in nearly $200k a year from a state pension? Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. NJ has one of the best pensions in the country (not saying anything about the funding level) and their pensions don't come close to that unless you possibly early 250k to 300k as a police admin. You forget she got to cash in 100 days of sick and vacation to hit her high 3 years of earning applied for pension. This is what long term financial planning and tax planning looks like. But ok. We’re doing it wrong. Oh. And when I retire I get to get on her health insurance plan for life. That’s why age 55 is the magic number. My severe service date, hers, all play into the financial plan we’ve been working our entire careers for. What KY pension system is that? Likely the one that’s only 16% funded. |

|

|

|

[#10]

Quoted: It's retraced back to March of 2019. But it can go down a lot further. Straw man argument. Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. |

|

|

|

[#11]

Quoted: It's retraced back to March of 2019.

|

|

|

|

[#12]

Quoted: I'm not sure you understand the definition of a straw man argument. Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. |

|

|

|

[#13]

Quoted: Quoted: Quoted: Quoted: stonk market is like a casino - rigged change my mind They did a study with monkeys who picked winning stocks over general day traders. It's definitely rigged. Build wealth, not get rich quick schemes. Pretty sure no such study has ever been conducted. I'd love to get a link to it though. https://www.forbes.com/sites/rickferri/2012/12/20/any-monkey-can-beat-the-market/?sh=446589b6630a https://www.wsj.com/articles/SB991681622136214659 Neither of those used monkeys. The first literally was just a random number simulator that they call a monkey as a reference to the malkiel quote. The wsj stock picks were actually just the staffers themselves throwing darts. |

|

|

|

[#14]

Quoted: Here's the meat: https://thereformedbroker.com/wp-content/uploads/2014/11/jpm_summer2013_rallc.pdf Quoted: Quoted: Quoted: Quoted: Quoted: stonk market is like a casino - rigged change my mind They did a study with monkeys who picked winning stocks over general day traders. It's definitely rigged. Build wealth, not get rich quick schemes. Pretty sure no such study has ever been conducted. I'd love to get a link to it though. https://www.forbes.com/sites/rickferri/2012/12/20/any-monkey-can-beat-the-market/?sh=446589b6630a https://www.wsj.com/articles/SB991681622136214659 Here's the meat: https://thereformedbroker.com/wp-content/uploads/2014/11/jpm_summer2013_rallc.pdf Again, no monkeys. They just used a random number generator to pick stocks. |

|

|

|

[#15]

Quoted: Again, no monkeys. They just used a random number generator to pick stocks. Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: stonk market is like a casino - rigged change my mind They did a study with monkeys who picked winning stocks over general day traders. It's definitely rigged. Build wealth, not get rich quick schemes. Pretty sure no such study has ever been conducted. I'd love to get a link to it though. https://www.forbes.com/sites/rickferri/2012/12/20/any-monkey-can-beat-the-market/?sh=446589b6630a https://www.wsj.com/articles/SB991681622136214659 Here's the meat: https://thereformedbroker.com/wp-content/uploads/2014/11/jpm_summer2013_rallc.pdf Again, no monkeys. They just used a random number generator to pick stocks. If I remember correctly, the r sqaure is more favorable on the non monkey picked portfolio, which may or may not matter to someone |

|

|

|

[#16]

Quoted: If I remember correctly, the r sqaure is more favorable on the non monkey picked portfolio, which may or may not matter to someone Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: stonk market is like a casino - rigged change my mind They did a study with monkeys who picked winning stocks over general day traders. It's definitely rigged. Build wealth, not get rich quick schemes. Pretty sure no such study has ever been conducted. I'd love to get a link to it though. https://www.forbes.com/sites/rickferri/2012/12/20/any-monkey-can-beat-the-market/?sh=446589b6630a https://www.wsj.com/articles/SB991681622136214659 Here's the meat: https://thereformedbroker.com/wp-content/uploads/2014/11/jpm_summer2013_rallc.pdf Again, no monkeys. They just used a random number generator to pick stocks. If I remember correctly, the r sqaure is more favorable on the non monkey picked portfolio, which may or may not matter to someone I demand nothing but the freshest monkeys. Straight from the rainforest too. None of this caged, farm raised bs. Wild caught. |

|

|

|

[#17]

MARKETS IN THE GREEN TODAY!!

woot woot!!!

|

|

|

|

[#18]

Buying will go up for a few days before next week when the fed rate hike of 1% knocks down the market 4-5%.

They will claim nobody saw it coming. |

|

|

|

[#19]

Quoted: Buying will go up for a few days before next week when the fed rate hike of 1% knocks down the market 4-5%. They will claim nobody saw it coming. That’s what happened yesterday. 75 was expected and known. Now 100 is on the table and likely. |

|

|

|

[#20]

|

|

|

|

[#21]

Quoted: Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. |

|

|

|

[#22]

Quoted: So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. Quoted: Quoted: Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. Good math. But you’re forgetting the 100 day sick/vacay payout that impacts high 3 payout. And we invest 50-60% of our take home after taxes. Spend way way less than you make. I have enough shit. 19500 into tax deferred times 2 = 51000 invested. Every. Fucking. Year. Hit age 50, 27500. 55,000 invested. Lowers taxable income. Grows tax free. That’s why I keep screaming max out your tax deferred options. Pay yourself first. Somebody making 120k allows them to just about max 401k at 15% |

|

|

|

[#23]

Quoted: So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. Quoted: Quoted: Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. Lots of pension plans have payouts that well exceed what they have collected. Various reports put the public pension shortfall anywhere from $5 trillion to $7 trillion. Austerity is coming, either via benefit cuts or via increased taxes. |

|

|

|

[#24]

Quoted: Lots of pension plans have payouts that well exceed what they have collected. Various reports put the public pension shortfall anywhere from $5 trillion to $7 trillion. Austerity is coming, either via benefit cuts or via increased taxes. Austerity is coming, either via benefit cuts or via increased taxes. BOTH!!! |

|

|

|

[#25]

Quoted: Good math. But you’re forgetting the 100 day sick/vacay payout that impacts high 3 payout. And we invest 50-60% of our take home after taxes. Spend way way less than you make. I have enough shit. 19500 into tax deferred times 2 = 51000 invested. Every. Fucking. Year. Hit age 50, 27500. 55,000 invested. Lowers taxable income. Grows tax free. That’s why I keep screaming max out your tax deferred options. Pay yourself first. Somebody making 120k allows them to just about max 401k at 15% Isn't it 20,500 each which is $41,000 plus dual $6,000 ROTHS for $53,000. Hit catchup contributions at 50 and it increases to $27,000 each for $54,000 total. Then $7,000 for ROTH each which will be $68,000 of tax advantages savings after 50. |

|

|

|

[#26]

Quoted: Good math. But you’re forgetting the 100 day sick/vacay payout that impacts high 3 payout. And we invest 50-60% of our take home after taxes. Spend way way less than you make. I have enough shit. 19500 into tax deferred times 2 = 51000 invested. Every. Fucking. Year. Hit age 50, 27500. 55,000 invested. Lowers taxable income. Grows tax free. That’s why I keep screaming max out your tax deferred options. Pay yourself first. Somebody making 120k allows them to just about max 401k at 15% Quoted: Quoted: Quoted: Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. Good math. But you’re forgetting the 100 day sick/vacay payout that impacts high 3 payout. And we invest 50-60% of our take home after taxes. Spend way way less than you make. I have enough shit. 19500 into tax deferred times 2 = 51000 invested. Every. Fucking. Year. Hit age 50, 27500. 55,000 invested. Lowers taxable income. Grows tax free. That’s why I keep screaming max out your tax deferred options. Pay yourself first. Somebody making 120k allows them to just about max 401k at 15% Spidey - if you are talking elective deferral to a 401k - it is $20,500 for 2022. $20,500 in 2022, $19,500 in 2020 and 2021, $19,000 in 2019, $18,500 in 2018, and $18,000 in 2015 - 2017. So a married couple both working with 401k's is $20,500 * 2 = $41000. Add $6500 for age 50+ catchup limit each takes it to $54,000 total Next - you said "Lowers taxable income. Grows tax free." That's not really correct. If you choose the pretax category - then it lowers your taxable income now, but grows tax deferred. If your plan offers Roth 401k and you choose that - it does NOT lower your taxable income now, but then it does grow tax free. |

|

|

|

[#27]

Quoted: Spidey - if you are talking elective deferral to a 401k - it is $20,500 for 2022. $20,500 in 2022, $19,500 in 2020 and 2021, $19,000 in 2019, $18,500 in 2018, and $18,000 in 2015 - 2017. So a married couple both working with 401k's is $20,500 * 2 = $41000. Add $6500 for age 50+ catchup limit each takes it to $54,000 total Next - you said "Lowers taxable income. Grows tax free." That's not really correct. If you choose the pretax category - then it lowers your taxable income now, but grows tax deferred. If your plan offers Roth 401k and you choose that - it does NOT lower your taxable income now, but then it does grow tax free. Quoted: Quoted: Quoted: Quoted: Before tax, pretty close. I view it as getting my taxes back. But understand about 15% of her compensation went to pension fund. Her entire career. If private professionals did that they’d have similar income. Out biggest expense by far are taxes. So I'm trying to figure this out. This isn't me trying to pick on your statements, just trying to understand so please I don't intend it to be combative. To withdraw roughly 16k per month pre tax after 27 years of investing 15% of pretax income, assuming you want to withdraw for 30 years, how much do you have to invest? Taking the (non inflation adjusted) average yearly return of the DOW from 1990-2020 (8.5%) and the inflation rate over that 30 year span (2.3%) you'd have to invest an average of ~$3850 per month. If that is 15% of your income you'd have to be making an average of over $257k per year over that span of time. That's not factoring in healthcare or insurance or anything else. These calculations are also assuming the rate of return will stay at that level and inflation will also stay at 2.3% going forward. No wonder the KY pension system is in such trouble. Edit - again to clarify this is an educational attempt for myself, these numbers could be from Bob down the street I'm just trying to figure out the economical reasonableness of this from an investment perspective. Good math. But you’re forgetting the 100 day sick/vacay payout that impacts high 3 payout. And we invest 50-60% of our take home after taxes. Spend way way less than you make. I have enough shit. 19500 into tax deferred times 2 = 51000 invested. Every. Fucking. Year. Hit age 50, 27500. 55,000 invested. Lowers taxable income. Grows tax free. That’s why I keep screaming max out your tax deferred options. Pay yourself first. Somebody making 120k allows them to just about max 401k at 15% Spidey - if you are talking elective deferral to a 401k - it is $20,500 for 2022. $20,500 in 2022, $19,500 in 2020 and 2021, $19,000 in 2019, $18,500 in 2018, and $18,000 in 2015 - 2017. So a married couple both working with 401k's is $20,500 * 2 = $41000. Add $6500 for age 50+ catchup limit each takes it to $54,000 total Next - you said "Lowers taxable income. Grows tax free." That's not really correct. If you choose the pretax category - then it lowers your taxable income now, but grows tax deferred. If your plan offers Roth 401k and you choose that - it does NOT lower your taxable income now, but then it does grow tax free. Thanks for the correction. It’s symantics. It does grow tax free, as in you pay no tax on growth. As in any yearly tax obligation. I pay a ton of taxes on my taxable account (DIV) and other cap gains. This does not happen in tax deferred accounts. Most my shit is in taxable accounts. And you know that tax deferred distributions are taxed as income. Not growth. Basis doesn’t matter. The basis was never taxed. Either way for people with a good income lowering taxable income is good. Our biggest expense bar none is quarterly tax payments. |

|

|

|

[#28]

FedEx stock tanks nearly 15% after company withdraws outlook, says year is about to get worse.

|

|

|

|

[#29]

Quoted: FedEx stock tanks nearly 15% after company withdraws outlook, says year is about to get worse. https://www.ar15.com/media/mediaFiles/140585/fdx_PNG-2527411.JPG Buy the fucking dip. Tomorrow is Friday. You know what happens every Friday without fail? My buy orders go in. Every. Fucking. Week. |

|

|

|

[#30]

Quoted: I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? IOW, How much of those “gains” are based on stimulus, and or Irrational Exuberance? 2800 might be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. - I’m not saying don’t invest. It’s something we have to do. I already put in the full $27000 into the 401k, and the company put in $31,000, Plus at least $5k a month just waiting to go to the taxable account. I just can’t see throwing good money after bad, when the Fed is clearly saying it’s time to pop the bubble. Don’t fight the Fed. |

|

|

|

[#31]

Quoted: It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. Quoted: Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I didn’t fight the fed. I used free money. Now that free money will grow. Inflation will raise stock price long term. So I’m still not fighting the fed. |

|

|

|

[#32]

Quoted: FedEx stock tanks nearly 15% after company withdraws outlook, says year is about to get worse. https://www.ar15.com/media/mediaFiles/140585/fdx_PNG-2527411.JPG FedEx and UPS is merging, the new company will be called FedUp!

|

|

|

|

[#33]

Quoted: Buy the fucking dip. Tomorrow is Friday. You know what happens every Friday without fail? My buy orders go in. Every. Fucking. Week. Good luck! |

|

|

|

[#34]

Quoted: Good luck! Quoted: Quoted: Buy the fucking dip. Tomorrow is Friday. You know what happens every Friday without fail? My buy orders go in. Every. Fucking. Week. Good luck! Fuck. I want another 4-5% drop tomorrow. That would be awesome. Why people are so scared to buy low is beyond me. If your scared of losing money, you’re scared of making money. Risk 101. |

|

|

|

[#35]

Quoted: And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I suspect the “Don’t time the Market” philosophy is left over Ancestor Worship, from the time where the Fed wasn’t so blatant in manipulating the Markets. I know they Have for a long time, but they used to be more circumspect and mysterious. The shit they did with Tarp, and then Covid; each was unprecedented and exponentially worse. Time will tell I guess. I still have ~2/3 of my money In, regardless, but I’m stacking cash. You aren't completely wrong about inflation eroding it, but you’re forgetting that, as the market drops, each dollar is getting bigger (ie.Deflation) My last big AAPL buy was at 133 this June. I’ll buy again when it gets closer to that. Problem is, I can’t think of any other AAPL’s. Any other companies spring to mind with similar earnings, growth and market share, etc? I truly think we could revisit 2007/2008, (not the raw numbers, but the perhaps a similar scale). They’re cranking up the lending rates so fast, it’s like they Want it to happen. People in our bracket, tend to forget what 3% to-> 6% does to the average family. Monthly mortgage payments nearly double, and that’s unsustainable, even for people who really want to buy. |

|

|

|

[#36]

Quoted: Why people are so scared to buy lower is beyond me. Fixed it for u. |

|

|

|

[#37]

Quoted: I suspect the “Don’t time the Market” philosophy is left over Ancestor Worship, from the time where the Fed wasn’t so blatant in manipulating the Markets. I know they Have for a long time, but they used to be more circumspect and mysterious. The shit they did with Tarp, and then Covid; each was unprecedented and exponentially worse. Time will tell I guess. I still have 2/3 of my money In, regardless. Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I suspect the “Don’t time the Market” philosophy is left over Ancestor Worship, from the time where the Fed wasn’t so blatant in manipulating the Markets. I know they Have for a long time, but they used to be more circumspect and mysterious. The shit they did with Tarp, and then Covid; each was unprecedented and exponentially worse. Time will tell I guess. I still have 2/3 of my money In, regardless. It’s funny you mentioned those times. That’s when I made my most money. By far. How? By not being scared. Well that’s not totally true. I made my most money when My President Trump was in office to cap off the greatest bull run in history. That’s why I give zero fucks if my value goes down 25%. I’ve been through bears before. It’s when you make the most money. |

|

|

|

[#38]

Quoted: It’s funny you mentioned those times. That’s when I made my most money. By far. How? By not being scared. Well that’s not totally true. I made my most money when My President Trump was in office to cap off the greatest bull run in history. That’s why I give zero fucks if my value goes down 25%. I’ve been through bears before. It’s when you make the most money. Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I suspect the “Don’t time the Market” philosophy is left over Ancestor Worship, from the time where the Fed wasn’t so blatant in manipulating the Markets. I know they Have for a long time, but they used to be more circumspect and mysterious. The shit they did with Tarp, and then Covid; each was unprecedented and exponentially worse. Time will tell I guess. I still have 2/3 of my money In, regardless. It’s funny you mentioned those times. That’s when I made my most money. By far. How? By not being scared. Well that’s not totally true. I made my most money when My President Trump was in office to cap off the greatest bull run in history. That’s why I give zero fucks if my value goes down 25%. I’ve been through bears before. It’s when you make the most money. Your “Cash getting eaten alive” comment is wrong, as it relates to buying stocks. When the Price is going down, the Dollar value goes up. But you already know that. I’m just pointing out the fact that Inflation doesn't impact everything, at the same speed and ferocity. Typically, Things you Need, get more expensive, things you don't need, get cheaper. Would you buy a House right now, if you didn’t absolutely need to? |

|

|

|

[#39]

Quoted: Your “Cash getting eaten alive” comment is wrong, as it relates to buying stocks. When the Price is going down, the Dollar value goes up. But you already know that. I’m just pointing out the fact that Inflation doesn't impact everything, at the same speed and ferocity. Typically, Things you Need, get more expensive, things you don't need, get cheaper. Would you buy a House right now, if you didn’t absolutely need to? Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I suspect the “Don’t time the Market” philosophy is left over Ancestor Worship, from the time where the Fed wasn’t so blatant in manipulating the Markets. I know they Have for a long time, but they used to be more circumspect and mysterious. The shit they did with Tarp, and then Covid; each was unprecedented and exponentially worse. Time will tell I guess. I still have 2/3 of my money In, regardless. It’s funny you mentioned those times. That’s when I made my most money. By far. How? By not being scared. Well that’s not totally true. I made my most money when My President Trump was in office to cap off the greatest bull run in history. That’s why I give zero fucks if my value goes down 25%. I’ve been through bears before. It’s when you make the most money. Your “Cash getting eaten alive” comment is wrong, as it relates to buying stocks. When the Price is going down, the Dollar value goes up. But you already know that. I’m just pointing out the fact that Inflation doesn't impact everything, at the same speed and ferocity. Typically, Things you Need, get more expensive, things you don't need, get cheaper. Would you buy a House right now, if you didn’t absolutely need to? Sure. People are spoiled by sub 4% interest rates. I sure as fuck locked my cash out refi at 3% for 30 years. That was super opportunity. Once in a lifetime. And 6-7%? Historically still pretty decent if you want to buy a house. Mortgage rates aren’t going to see that opportunity again. Your house is not a source of wealth. It’s an illiquid appreciating asset with expense. Nothing more, nothing less. |

|

|

|

[#40]

Quoted: Likely the one that’s only 16% funded. That’s what long term financial planning looks like. |

|

|

|

[#41]

Quoted: I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. Sorry, was a mistake. I meant March 2021. Funny you are the guy who said bear markets last 11 months, saying people can't read a chart and using ad hominems. |

|

|

|

[#42]

Another day, another drop in the Sp500. Spidey started this thread at 4200, and recommended catching a falling knife off that dead cat bounce all the way through today at 3900.

|

|

|

|

[#43]

Quoted: Another day, another drop in the Sp500. Spidey started this thread at 4200, and recommended catching a falling knife off that dead cat bounce all the way through today at 3900. And I’ll keep buying every fucking Friday a set amount. Every fucking week. Small swings don’t impact what I do. Now big huge swings do. I just buy more. It’s how you make the most money. I WANT it to go down. |

|

|

|

[#44]

Quoted: Fuck. I want another 4-5% drop tomorrow. That would be awesome. Why people are so scared to buy low is beyond me. If your scared of losing money, you’re scared of making money. Risk 101. obviously i can't speak for everyone else, but my fear is that one of these times it will take decades to recover in real terms. There have been multiple, decade long periods for markets to recover in real terms. Even with the drop in the markets this year, stocks are still historically overpriced, and markets tend to swing like pendulum between overvalued and undervalued. But i guess that depends on what you consider "low." And yes, the value of cash is being destroyed by inflation, but as Rick Rule has said, you need to have some cash, and think of the erosion of your purchasing power as an option premium. If there is a liquidity crisis like in 2008 and 2020, you can take advantage of the panic instead of being taken advantage of. I'm ready for whatever happens. I contribute to my 401k every 2 weeks to a SP500 fund, as well as hold cash, bonds, and commodities (specifically uranium). |

|

|

|

[#45]

|

|

|

|

[#46]

My Robinhood account has it at $165ish. My Fidelity shows at $204. |

|

|

|

[#47]

Quoted: My Robinhood account has it at $165ish. My Fidelity shows at $204. Quoted: My Robinhood account has it at $165ish. My Fidelity shows at $204. Robinhood is showing after hours. Fidelity is showing yesterday's close. Debt killed FedEx's EPS. Higher interest rates are going to slaughter companies that roll debt over cyclically. |

|

|

|

[#48]

Quoted: And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I didn’t fight the fed. I used free money. Now that free money will grow. Inflation will raise stock price long term. So I’m still not fighting the fed. Quoted: Quoted: Quoted: Quoted: Quoted: Quoted: ZOMG! The S&P has retraced all the way back to where it was 6 days ago!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!! SELL! SELL! SELL! It's retraced back to March of 2019. But it can go down a lot further. Quoted: 1. If this is so clear, why doesn't every market analyst who does this for a living agree with you? 2. In 2010-2011, we had a LOT of Arfcom experts saying the same thing, all during the market bull run. Straw man argument. I'm not sure you understand the definition of a straw man argument. I’m convinced doomers can’t read a chart. March 2019 was 2800. For the math impaired that means if you bought March 2019, you have 33% gains in a little over 3 years. It’s interesting how the Pessimist vs. Optimist mindset works. You look at that chart and say, woohoo,I’m still up 33%!!! I look at the exact same chart and think “How far can this fall, without all the Fed (free money) support? 2800 would be a pretty good All-In buy point, considering all the inflation we’ve had. I’m buying back a little at a time now, and when we get to ~3400 I’m going to pick it up. If we get to 3000 it’s time to start going full Spidey. And what is happening to your cash now? Getting eaten alive. Full spidey is not attempting to time and just keep buying every fucking week. Market up? Buy Market down bigly? Buy more I didn’t fight the fed. I used free money. Now that free money will grow. Inflation will raise stock price long term. So I’m still not fighting the fed. Money is never free. |

|

|

|

[#49]

Quoted: Robinhood is showing after hours. Fidelity is showing yesterday's close. Debt killed FedEx's EPS. Higher interest rates are going to slaughter companies that roll debt over cyclically. https://www.ar15.com/media/mediaFiles/200878/FedEx_JPG-2527935.JPG Quoted: Quoted: My Robinhood account has it at $165ish. My Fidelity shows at $204. Robinhood is showing after hours. Fidelity is showing yesterday's close. Debt killed FedEx's EPS. Higher interest rates are going to slaughter companies that roll debt over cyclically. https://www.ar15.com/media/mediaFiles/200878/FedEx_JPG-2527935.JPG reasonable p/e and dividend. Sorta want.  |

|

|

|

[#50]

Quoted: reasonable p/e and dividend. Sorta want. Quoted: Quoted: Quoted: My Robinhood account has it at $165ish. My Fidelity shows at $204. Robinhood is showing after hours. Fidelity is showing yesterday's close. Debt killed FedEx's EPS. Higher interest rates are going to slaughter companies that roll debt over cyclically. https://www.ar15.com/media/mediaFiles/200878/FedEx_JPG-2527935.JPG reasonable p/e and dividend. Sorta want. People are still gonna order shit....And we are on the precipice of Santa Time. |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.