|

[#1]

Quoted: I think you understand the situation far better than most, and yep..... I also agree most things right now need a 30% correction to be healthy, and I think that would happen in a hart beat, I think it would be closer to 40% personally. But I am scared they (the fed) doesn't have the stones for that, and there friends in the big banks would loose some money, and they can't have that. Sooooo... savers and the little guy will get tossed under the buss. My other thought is, they might just do it, and let everything take a 30-40% hit, to slow inflation, if they think it will kill crypto and remove that possible competition to the fed system. We have came up with a few ways to protect some money in this thread. 10k in those Treasury Direct I bonds at 7% is something I was sure glad to learn about, and learned about it from this thread. So side question. We covered some places to move some money. What about everyone with 401k's and what could one do to help protect that? Most plans are just target date funds, bond funds, or market index funds. To me all 3 of those are NOT the place to be if there is a correction. Mine had a choice for a T bill but NOT really T bills option, it's a insurance instrument to mimic t bills. I jumped to that at the end of the year. Right now I am just sorta waiting to see what that first rate hike is, and if they really go to 0 on the taper and if they start to sell anything off there balance sheet. Or if it's all BS, if BS I am jumping back in, to ride the bull. To me that's the tell, and we won't know till they do it or not. Bonds I guess |

|

|

|

[#2]

Quoted:  Then maybe it is just you investing wrong. Go ahead and list 10 stocks that have lost 50% of their value in the last year. Then maybe it is just you investing wrong. Go ahead and list 10 stocks that have lost 50% of their value in the last year.He’s right 40% of the NASDAQ is down 50% of their 52 week highs |

|

|

|

[#3]

Quoted: cutting the power to your house does not mean electricity somehow stop being a thing for other building. just like blocking access from one computer to google.com in no way means google.com ceases to exist  some of you almost unbelievably ignorant. Someone has to be the other side of the trade.  |

|

|

|

[#4]

Quoted: Bonds I guess I wouldn't go into bonds.... From what I understand right now the bond market is even more F ed up than the stock market..... But I don't understand the bond market at all.... NOPE to the bonds at least for me. that treasury direct I bond is a different animal from the "bond market" you will get in your 401k. And I haven't a clue if you could get 401k money into it and it's capped at 10k per person per year anyways. I don't know where to go... that's why I am so active in this thread, and 401k's make it even harder. I am trying to figure out the same thing and get as many ideas as I can. I am NOT the guy to get financial advice from, I lost over 2 million back in 08, I dam near got wiped out. I made the wrong calls in that one, and am just now starting to recover from it, I don't want to do that again. I am NOT giving financial advice, I am a clueless nob trying to learn. @gmtech and @OregonShooter |

|

|

|

[#5]

Quoted: Someone has to be the other side of the trade. lol exactly my point, hell that might even be me offering to buy some pore bastards Bit coin at $2,501.51 each. People don't think "market orders" be like they do.... but.... When I was young I traded futures and got trapped on the wrong side of 2 coffee contracts for 3 DAYS of lock limit moves. I had a market order in every day to get out of my position but didn't get filled... Took me 3 days to get filled.... And near as I can tell cryptos don't have limits (shutter......). Hope you run into some limit buy orders setting there as she free falls. Hmmmmmmm |

|

|

|

[#6]

tag, seems like a solid thread with a lot of good info!

|

|

|

|

[#7]

Quoted: Like the sub-prime issue a few years ago, they will find a way to cook the books and kick the can down the road again Quoted: Quoted: They can't. Any meaningful increase will bring about bankruptcies. The US government can't afford to service its debt, yet alone try to pay it off (El Oh El). The Too Big To Fail/Jail crowd can't survive either as they rely on cheap currency to survive. Any decrease/tapering will also be meaningless. What? .25 of one percent? El Oh El again. The entire fiat currency system is based on an expanding currency supply until it doesn't work; at which point it collapses. We're near that point now and if you know fiat currency history, you would know that fiat currencies historically lasts only 40-50 years. We're past the 50 year mark and that's a pretty good run; but when it's over, it's over. Unfortunately its demise will destroy a large part of the middle class (which was on intent) as wealth is not destroyed but transferred and in this case, upwards. Don't let this happen to your grandchildren yet to be born. End the Fed. End their power over us. Stop the thefts. I have zero faith of gov fixing anything. Any attempt to fix these problems will cause unhappy people, and gov is playing santa claus as a method of ruling. They wont be responsible for bad job numbers, bad market numbers, etc, so yeah, kick the can until its impossible to kick it another inch. Democrats wont let the fed raise rates if it will make them look bad, not a chance. A repub win in 2024 ? Yeah, rates will skyrocket if a repub is in charge, as all blame will go to the repub. Just remember....theres no one in charge willing to do " the right thing " or whats right for the usa....they will put themselves and their party first, were being ruled by corrupt idiots, just plan around that fact. They are addicted to spending money as well, so expect trillion buck bill after trillion buck bill to be sponsored. Whatever earns them more money and results in the least amount of push back politically, thats what they will do. |

|

|

|

[#8]

40% of the NASDAQ 50% off their high. Only a handful of mega caps holding up the party.

|

|

|

|

[#9]

10 stocks 50% or more off their high.

Docusign GameStop AMC Macys…35% Robinhood Palantir Viacom Penn National Gaming Zoom Good RX Moderna Traeger Etherium/Bitcoin off 40% Quoted: Then maybe it is just you investing wrong. Go ahead and list 10 stocks that have lost 50% of their value in the last year. |

|

|

|

[#10]

No place to go or hide, let the pain commence.

|

|

|

|

[#11]

Quoted: No place to go or hide, let the pain commence.  |

|

|

|

[#12]

Quoted: tag, seems like a solid thread with a lot of good info! Yep, great thread and contributors. Needs some @jaqufrost to round it out. |

|

|

|

[#13]

Quoted: So I'm supposed to move the 401K out of stocks and into bonds.... Bonds are down 200 basis points since December 22, I wouldn’t recommend that. What I would do is move to more boring stocks for a Safeharbor for the year |

|

|

|

[#14]

Quoted: +1 Thank you for that info. Quoted: Quoted: Quoted: I like I bonds from treasury direct.gov right now paying 7% and you can get 10k per year per family member. Its a good safe place otherwise I'd shift out of unrealistic bullshit. I like some commodity for inflation hedge, consumer staples, telecom, and energy, they will suffer too but not like meme stocks will. As for buying a home some markets are still semi affordable others I'd just avoid. THANK YOU for that. I didn't even think of that, shows how much I know... I am digging into it a little right now. I may be buying some of those. Near as I can tell. After one year I can cash it out, so not totally trapped. And from year 1-5 I lose 3 months int for early withdraw penalty. But shit those rates (even with a 3 month loss of int) still beat anything else out there right now for a CD like product. BUT the thing is, if there is a big market correction, I would like to be able to move in and snap some things up that are on sale.... and don't want locked in for one year. BUT this is a limited about, and a good way to diversify some cash so probably going to buy some. Thanks again. same, i had no idea those existed. |

|

|

|

[#15]

Trees don't grow to the sky forever. Reality is sinking in.

|

|

|

|

[#16]

Quoted:Yep, great thread and contributors. Needs some @jaqufrost to round it out. I'm not sure how much I have to add. The Fed appears to be trapped into keeping interest rates fairly low. I believe they find inflation to be more acceptable than depressions. Normally this is heavily offset by the deflationary nature of technological progression, but not so much the last 24 months. Short term we could head into a recession, but longer term the Fed will print more trying to get out of the down turn and push inflation back up. As far as the government debt goes, it's a bit of a self licking ice cream cone. Dollars borrowed below the real inflation rate get spend increasing inflation and making the previously borrowed money easier to pay back. So IMO the can can be kicked for some time. I'll be looking for ways to leverage if Shiller P/E drops, but right now I'm not going to take a loan out on my home to buy the market. Always be careful with leverage and make sure you don't get too illiquid and wiped out. |

|

|

|

[#17]

Quoted: I'm not sure how much I have to add. The Fed appears to be trapped into keeping interest rates fairly low. I believe they find inflation to be more acceptable than depressions. Normally this is heavily offset by the deflationary nature of technological progression, but not so much the last 24 months. Short term we could head into a recession, but longer term the Fed will print more trying to get out of the down turn and push inflation back up. As far as the government debt goes, it's a bit of a self licking ice cream cone. Dollars borrowed below the real inflation rate get spend increasing inflation and making the previously borrowed money easier to pay back. So IMO the can can be kicked for some time. I'll be looking for ways to leverage if Shiller P/E drops, but right now I'm not going to take a loan out on my home to buy the market. Always be careful with leverage and make sure you don't get too illiquid and wiped out. How about some volatility bets? |

|

|

|

[#18]

Quoted: How about some volatility bets? I'm interested in hearing your ideas. |

|

|

|

[#19]

Quoted: Bonds are down 200 basis points since December 22, I wouldn’t recommend that. What I would do is move to more boring stocks for a Safeharbor for the year Quoted: Quoted: So I'm supposed to move the 401K out of stocks and into bonds.... Bonds are down 200 basis points since December 22, I wouldn’t recommend that. What I would do is move to more boring stocks for a Safeharbor for the year I don't see a lot of great options here and I think this is typical. |

|

|

|

[#20]

They'll do it once and then when the wheels fall off they'll walk back like they did during that 2018 dip.

|

|

|

|

[#21]

|

|

|

|

[#22]

Quoted: https://pbs.twimg.com/media/FHuujxiXoAk_0-D?format=jpg&name=large Straight price isn't a good way to analyze whether it's a bubble. Shiller P/E is better. 2008 wasn't nearly as much of a bubble as 1999. Todays bubble is about inline with the 99 bubble. |

|

|

|

[#23]

Quoted: Straight price isn't a good way to analyze whether it's a bubble. Shiller P/E is better. 2008 wasn't nearly as much of a bubble as 1999. Todays bubble is about inline with the 99 bubble. The money for those earnings is also printed... stop creating that money and what will justify those P/E ratios? |

|

|

|

[#24]

Quoted: The money for those earnings is also printed... stop creating that money and what will justify those P/E ratios? The Fed can't stomach long term deflation. I don't see the money printers stopping for any long period of time. |

|

|

|

[#25]

Quoted: The Fed can't stomach long term deflation. I don't see the money printers stopping for any long period of time. Most money is created by banks, not the fed, so the only way to keep creating money is to keep banks lending. Which is why we've kept inflating the asset bubble. Raise interest rates and you'll cause deleveraging, which means money will be "destroyed" by being paid back into the banks. |

|

|

|

[#26]

How else do you combat inflation?

|

|

|

|

[#27]

Quoted: Most money is created by banks, not the fed, so the only way to keep creating money is to keep banks lending. Which is why we've kept inflating the asset bubble. Raise interest rates and you'll cause deleveraging, which means money will be "destroyed" by being paid back into the banks. Yep, Deleveraging will happen, fed gets to pick if it happens via deflation or inflation. They will pick inflation since it benefits the borrowers (fed gov). |

|

|

|

[#28]

Quoted: Straight price isn't a good way to analyze whether it's a bubble. Shiller P/E is better. 2008 wasn't nearly as much of a bubble as 1999. Todays bubble is about inline with the 99 bubble. Quoted: Quoted: https://pbs.twimg.com/media/FHuujxiXoAk_0-D?format=jpg&name=large Straight price isn't a good way to analyze whether it's a bubble. Shiller P/E is better. 2008 wasn't nearly as much of a bubble as 1999. Todays bubble is about inline with the 99 bubble. The mantra is P/E is outdated and valuations are meaningless. I cringe every time I hear that valuations are irrelevant. |

|

|

|

[#29]

Quoted: I'm interested in hearing your ideas. Quoted: Quoted: How about some volatility bets? I'm interested in hearing your ideas. I'm working on some plans, nothing solid yet although anything in this space will be extreme risk. |

|

|

|

[#30]

Quoted: Straight price isn't a good way to analyze whether it's a bubble. Shiller P/E is better. 2008 wasn't nearly as much of a bubble as 1999. Todays bubble is about inline with the 99 bubble.

|

|

|

|

[#31]

|

|

|

|

[#32]

Quoted: Bonds are down 200 basis points since December 22, I wouldn’t recommend that. What I would do is move to more boring stocks for a Safeharbor for the year Problem is with most 401ks your choices are very limited. In your opinion what are good boring stocks to look at ? |

|

|

|

[#33]

Quoted: The Fed can't stomach long term deflation. I don't see the money printers stopping for any long period of time. Quoted: Quoted: The money for those earnings is also printed... stop creating that money and what will justify those P/E ratios? The Fed can't stomach long term deflation. I don't see the money printers stopping for any long period of time. Asset deflation or price deflation? I think they can tolerate asset deflation and have made the mistake of thinking price deflation is bad and have now been forced into a box where fighting price inflation will require asset deflation. Price deflation was never a bad thing in the modern economy. It is the cause of the deflation in price that can be good or bad, but the fed has not allowed any regardless of reason. |

|

|

|

[#34]

Quoted: How about some volatility bets? I would also love to hear some ideas on this. |

|

|

|

[#35]

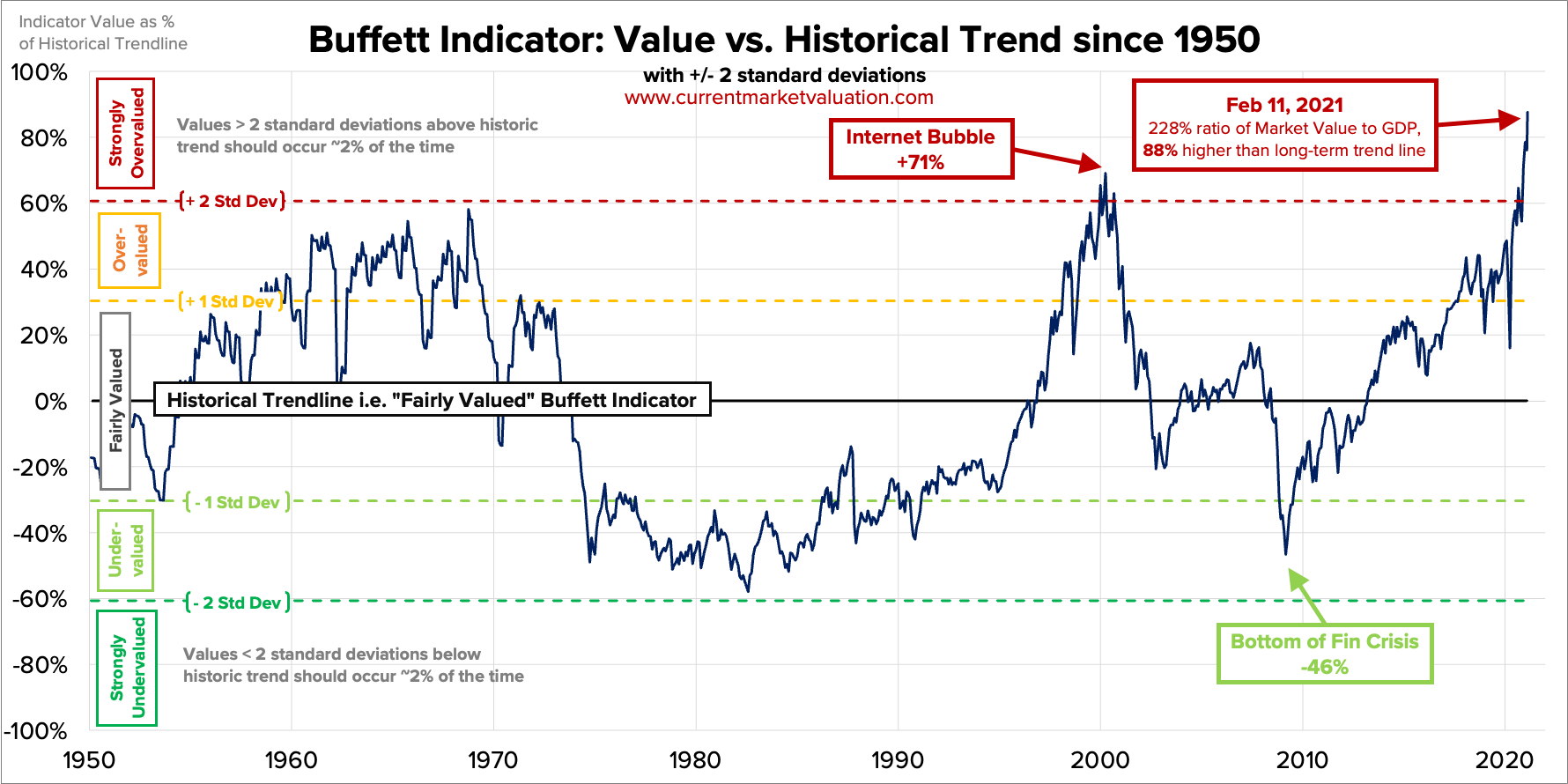

Thanks for sharing those charts SquirrleAssassin. That is interesting. My take is they are showing a explosion of prices of the market and of ammonia that matches with massive amounts of money being pumped into the system. That Buffet chart makes me think it's another bubble, but your first chart is saying NOT a bubble. So not sure what you are saying with that. Looks like a bubble on roids to me, or a market crashing though the roof from a currency failure. What is your take? |

|

|

|

[#36]

Quoted: I would also love to hear some ideas on this. Quoted: Quoted: How about some volatility bets? I would also love to hear some ideas on this. Then you play the bear short game. High high risk, high reward though. I want nothing to do with short term stuff. |

|

|

|

[#37]

Quoted: Then you play the bear short game. High high risk, high reward though. I want nothing to do with short term stuff. lol yep... scares me more than going long in the market today. But I always love hearing peoples ideals and the more ways you know to hedge or tie things together the better. Like I told about getting on the wrong side of a pair of coffee futures contracts, and getting stuck for 3 days of limit moves... OUCH. It's scary how fast some things can move and lock up and you can't get out. |

|

|

|

[#38]

Quoted: they can't. they won't. This is what I think. I believe that they're floating the idea of raising interest rates now so that when they do it, the market already has it factored in and the hit will be less. The issue is that they've essentially ruined saving. |

|

|

|

[#39]

Quoted: lol yep... scares me more than going long in the market today. But I always love hearing peoples ideals and the more ways you know to hedge or tie things together the better. Like I told about getting on the wrong side of a pair of coffee futures contracts, and getting stuck for 3 days of limit moves... OUCH. It's scary how fast some things can move and lock up and you can't get out. Quoted: Quoted: Then you play the bear short game. High high risk, high reward though. I want nothing to do with short term stuff. lol yep... scares me more than going long in the market today. But I always love hearing peoples ideals and the more ways you know to hedge or tie things together the better. Like I told about getting on the wrong side of a pair of coffee futures contracts, and getting stuck for 3 days of limit moves... OUCH. It's scary how fast some things can move and lock up and you can't get out. I’m long term permabull investor. I looked into margin loans/trading for tax reasons. Nope. Nope. Nope. Nope. I’ll stick to what I know. I like risk, but that was way too much for me. I’ll just be a boring turtle. |

|

|

|

[#40]

Quoted: This is what I think. I believe that they're floating the idea of raising interest rates now so that when they do it, the market already has it factored in and the hit will be less. The issue is that they've essentially ruined saving. Quoted: Quoted: they can't. they won't. This is what I think. I believe that they're floating the idea of raising interest rates now so that when they do it, the market already has it factored in and the hit will be less. The issue is that they've essentially ruined saving. Investing is saving. Where else you gonna get a return? |

|

|

|

[#41]

Quoted: I would also love to hear some ideas on this. Buy SPXS when you think the market will go down and SPXL when you think it'll go up. Or just say F it, refinance your house, use all proceeds to buy and hold SPXS all the way to the bottom. These don't require margin. You can only lose what you put into the stock price. |

|

|

|

[#42]

In before people who were not alive during 20% interest rates and don't think they are a thing.

Oh, too late. |

|

|

|

[#43]

Quoted: In before people who were not alive during 20% interest rates and don't think they are a thing. Oh, too late. +1 I just caught up on this thread and it’s clear there’s hobbyist finance bros that are about to get their faces ripped off. Dudes who think a big drop and 3-12mo recovery is bad. Get ready for a real rotational bear market boys because 2020 wasn’t a bear market. You don’t designate things with arbitrary percentage threshold breaches. And another thing- diversification doesn’t mean holding the same asset class across sectors and industries. You need to hold several different asset classes entirely. BUt sTOnKs OnLY gO uP |

|

|

|

[#44]

Quoted: In before people who were not alive during 20% interest rates and don't think they are a thing. Oh, too late. I don't think they can raise it that high the effects would be catastrophic. |

|

|

|

[#45]

Quoted: In before people who were not alive during 20% interest rates and don't think they are a thing. Oh, too late. Business cycles don’t care about their feels. Hell, I’ve started seeing girls wearing legit 70’s bell bottoms, and dudes looking like girls is coming back in fashion. Once you add Jimmy Carter after three sheets of acid as President. Is stagflationary pain amidst an energy crunch and escalating interest rates that far off the table? Lol |

|

|

|

[#46]

Quoted: I don't think they can raise it that high the effects would be catastrophic. Quoted: Quoted: In before people who were not alive during 20% interest rates and don't think they are a thing. Oh, too late. I don't think they can raise it that high the effects would be catastrophic. |

|

|

|

[#47]

Quoted: +1 I just caught up on this thread and it’s clear there’s hobbyist finance bros that are about to get their faces ripped off. Dudes who think a big drop and 3-12mo recovery is bad. Get ready for a real rotational bear market boys because 2020 wasn’t a bear market. You don’t designate things with arbitrary percentage threshold breaches. And another thing- diversification doesn’t mean holding the same asset class across sectors and industries. You need to hold several different asset classes entirely. BUt sTOnKs OnLY gO uP YEP.... lol and why I am so active on the topic... Do please go on. I was 80% RE 12% stocks 5% cash 3% commodities/PM I changed to 80% RE 17% cash 3% commodities/PM And being in a inflationary environment it KILLS me to know that 17% is getting eaten away by inflation. I know that, if rates get to high... I am apt to get my face ripped off on that RE as well. BUT at this time I can leverage more against the RE at a good rate, if I could figure somewhere to put it. Or I could sell and pay LTCG on some of it, but again where to put the money that would beat the RE. BUT I don't think RE in my area has peeked yet, and I do have rental cashflow. But that worm can turn quick. I feel like we might be going into a scary time, and I want to have my whits about me and make the right choices. The days of 20% int are before my time, but I remember dad telling about buying bonds for a discount when something like this happened, then earning 18% on the bonds for years and as it started to come out of it. Sold the bonds at a premium, plus kept the 18% it payed him though that time. But I have never played with bonds, they have been a dog my entire life, and from what I hear a house of cards from all the fed buying of them for years. |

|

|

|

[#48]

Quoted: Aside from rates, they need to stop buying stuff. FED needs to completely stop, not just slow down, buying Treasury debt and mortgage-backed securities. The market distortion is huge because of the Fed. And boy, would the Gov have a problem if they couldn't print money to pay their expenses. That will stop when the dollar is no longer the world currency. |

|

|

|

[#49]

Quoted: I don't see a lot of great options here and I think this is typical. https://www.ar15.com/media/mediaFiles/76/options_JPG-2235717.JPG Yep.... I have a chunk in a 401k that has even less choices than that. I just moved into the "stable value" option, there was only one. In my plan it was listed as a "insurance instrument". Set to "mimic t bills". Now how well it does that, and if they aren't just out gambling with it on the side, time will only tell. Yours is listed as "bond fund", you might dig into what they are holding. But I really don't have a clue... that's why trying to get group think on this. |

|

|

|

[#50]

Quoted: Yep.... I have a chunk in a 401k that has even less choices than that. I just moved into the "stable value" option, there was only one. In my plan it was listed as a "insurance instrument". Set to "mimic t bills". Now how well it does that, and if they aren't just out gambling with it on the side, time will only tell. Yours is listed as "bond fund", you might dig into what they are holding. But I really don't have a clue... that's why trying to get group think on this. Quoted: Quoted: I don't see a lot of great options here and I think this is typical. https://www.ar15.com/media/mediaFiles/76/options_JPG-2235717.JPG Yep.... I have a chunk in a 401k that has even less choices than that. I just moved into the "stable value" option, there was only one. In my plan it was listed as a "insurance instrument". Set to "mimic t bills". Now how well it does that, and if they aren't just out gambling with it on the side, time will only tell. Yours is listed as "bond fund", you might dig into what they are holding. But I really don't have a clue... that's why trying to get group think on this. My group think is you shouldn’t be finger fucking your 401k trying to time the market and stick to a long term risk investment strategy. Your risk tolerance is your own. If shit crashes, I’ll be happy as shits on sale. |

|

|

Win a FREE Membership!

Win a FREE Membership!

Sign up for the ARFCOM weekly newsletter and be entered to win a free ARFCOM membership. One new winner* is announced every week!

You will receive an email every Friday morning featuring the latest chatter from the hottest topics, breaking news surrounding legislation, as well as exclusive deals only available to ARFCOM email subscribers.

AR15.COM is the world's largest firearm community and is a gathering place for firearm enthusiasts of all types.

From hunters and military members, to competition shooters and general firearm enthusiasts, we welcome anyone who values and respects the way of the firearm.

Subscribe to our monthly Newsletter to receive firearm news, product discounts from your favorite Industry Partners, and more.

Copyright © 1996-2024 AR15.COM LLC. All Rights Reserved.

Any use of this content without express written consent is prohibited.

AR15.Com reserves the right to overwrite or replace any affiliate, commercial, or monetizable links, posted by users, with our own.